< Back to Articles | Time to Read: 5 minutes

A lift in the loan limits for the country’s most popular loans is great news for home shoppers in 2024. This increase reflects the growing average cost of homes, allowing more home buyers to borrow within the newly capped amount to avoid getting jumbo loans (which typically come with higher interest rates). The result is beneficial to those looking to purchase a home in 2024.

How do conforming loan limits work?Each year, a conforming loan limit is set by housing finance agencies Fannie Mae, Freddie Mac, and Ginnie Mae’s federal regulator, the Federal Housing Financing Agency (FHFA). A large portion of mortgages in the U.S. are backed by these agencies, which makes these loan limits an important part of the home buying process.

Conforming loan limits are based on median home values—which can vary from county to county across the U.S. So, typically, as home prices rise, loan limits will too. This allows home buyers to continue to keep up with the real estate market.

Look at the numbers.The FHFA announced the conforming loan limit will rise by $40,350 for most counties in the U.S. Loan limits were raised to help with an increase in home prices (in the last 24 months). This is the eighth straight year the conforming loan limits have been raised after not increasing from 2006-2016.

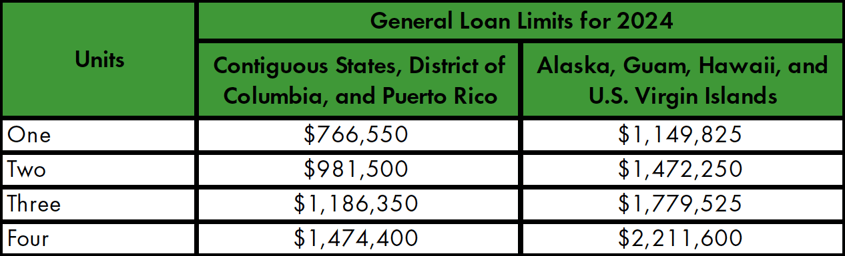

Starting January 1, 2024, the new limit is $766,550 for one-unit dwellings, which is an increase of $40,350 (or about 5.5% over the 2023 limit of $726,200). Per the FHFA, special statutory provisions establish different loan limit calculations for high-cost areas such as Alaska, Hawaii, the U.S. Virgin Islands, and Guam. In those areas, the baseline loan limit will be $1,149,825 for one-unit properties. This is great news for home buyers who may not want to enter into a jumbo loan for their next mortgage.

General Loan Limits for 2024:

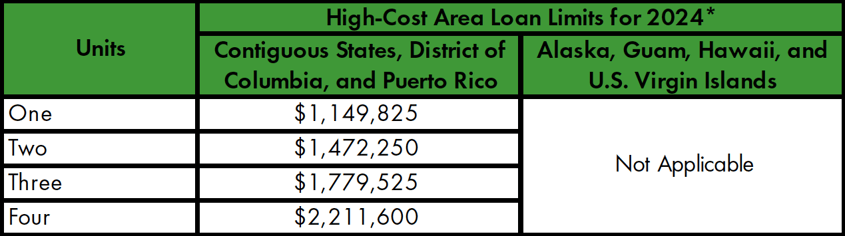

*Click here to see all 2024 conforming and high balance loan limits by county.

What’s the difference between conforming loans and jumbo loans?

If you borrow more than the conforming loan limit that’s allowed in your county, you’ll need to apply for a jumbo loan. Jumbo loans (also known as non-conforming loans) are privately backed mortgages that usually require a larger down payment, higher credit scores, and higher income levels from borrowers.

Consider the whole package when looking for a new home.With the tightening of the housing inventory, lack of starter homes in many U.S. real estate markets, and fluctuation of interest rates, it’s important to take a look at your whole financial picture. These are all things that can be assumed to be a barrier to buying a home. Break down some of these barriers and find an expert Home Loan Specialist who can walk through your personalized Homeowner Strategy Plan to provide you with:

- A budget breakdown

- Your down payment options

- An outline of the smartest loan products, interest rates, and terms

- Financial goal setting (for both short-term and long-term objectives)

For more information about 2024 conforming loan limits or how to start the home buying process, reach out to one of our Home Loan Specialists today.