< Back to Articles | Time to Read: 5 minutes

When you first bought your home, you probably took advantage of whatever option made the most sense at the time. For a lot of homeowners, that means taking on a 30-year mortgage. But what happens when it’s years later and you don’t feel like you’re making any progress in paying down your home loan or building up equity?

The fact is your current mortgage could be keeping you poor. But guess what? We can help you change that.

Refinancing can be key in saving money and building equity if you do it right.

You’re likely aware of the historically low interest rates available for home buyers right now. These rates are available to those of you who already own, as well. Before you jump into refinancing though, there’s some things you need to know.

Refinancing will only save you money if you do so in a way that makes sense. For example: Replacing your current 30-year mortgage with another 30-year mortgage? That just doesn’t make sense.

Why?

Even if your interest rate is lower, odds are that tacking on another three decades of payments to your mortgage won’t save you money in the long run. We want you to pay less AND own your home more quickly, not be stuck making house payments longer than necessary!

Exception: If you plan on selling in the next few years, refinancing for another 30-year mortgage at a lower rate could be beneficial, depending on the interest rate. Your Churchill Home Loan Specialist will be able to walk you through all your options and help you decide what’s right for you.

I want to speak to a Home Loan Specialist about refinancing!

What should you do instead?

The best option for refinancing is doing so at a lower rate and for a shorter time frame. The shorter loan will likely have a higher monthly payment, but it’s important to look at the overall total of the mortgage, not just what you will pay each month. Remember, by cutting the number of payments in half, you’ll save an incredible amount in interest over the life of your loan!

Right now, rates are still unbelievably low, and most homeowners could benefit from refinancing.

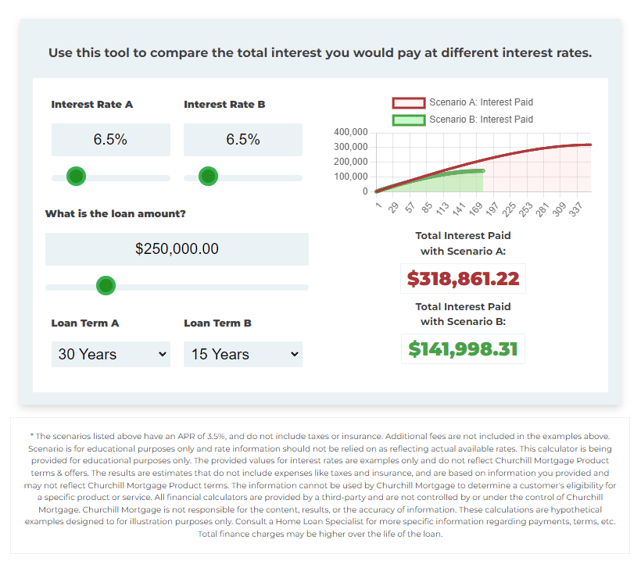

Let’s look at an example of how you could save money on a 15-year mortgage versus a 30-year mortgage. Interest rates for a 15-year loan term are typically lower than a 30-year loan term. So, if your original loan amount was $350,000 and you now want to refinance the balance of $225,000, you could save substantially (even if you factor in closing costs) by choosing a 15-year mortgage.

Every refinance looks different, so it’s important to know your current loan balance, loan term, and interest rate. That way you’ll be able to see where you can adjust your mortgage and save money by refinancing.

The money you save from interest could be the down payment on an investment property, your child’s college education, or a contribution toward retirement. No matter what you choose to do with the money you save, being a debt-free homeowner 15 years sooner can be life changing!

The money you save from interest could be the down payment on an investment property, your child’s college education, or a contribution toward retirement. No matter what you choose to do with the money you save, being a debt-free homeowner 15 years sooner can be life changing!

Now that you see how much you could save, let’s talk about the costs you might need to consider before refinancing.

- Appraisal Fee. An appraisal will most likely take place to figure out the current value of the home. These fees vary but see an average of $300-$600.

- Credit Report Fee. Your credit will be pulled by your lender, resulting in a charge. This is usually around $40.

- Lender Origination Fees. This fee is for underwriting and processing your home loan. It will vary depending on the mortgage company you work with.

- Attorney Fee. If a lawyer is required to review the paperwork for your mortgage, you will be charged a fee. The amount will vary based on the attorney you use.

Overall, homeowners can expect to spend about 2-4% of the amount of their home loan when refinancing. Figuring out the total closing costs before you choose to refinance with a lender is important in determining when you will break even. This will help you to decide if refinancing is right for you.

Keep an eye on interest rates with Rate Watch!

Recently, Fannie Mae and Freddie Mac changed their refinance guidelines. This has created the opportunity for more homeowners to refinance. If you were recently unable to get approved for a refinance, we’re here to help!

Fannie Mae’s RefiNow*

- If your mortgage is currently owned by Fannie Mae or Freddie Mac

- Your income is at or below of 100% of the Area Median Income limit for where your home is located

- Your mortgage is has been open at least 12 months

- You are lowering your interest rate at least 0.50% and your mortgage payment is going down

- Your mortgage payment has been paid on time

- Your credit score is at least 620

- Your debt-to-income ratio is 65% or less

- If an appraisal is required, you will receive a $500 credit

Your home is the biggest investment you’ll make, but that doesn’t mean you need to be financially limited because of it. We want to make sure you’re making the best decisions for you, your family, and your future. You can count on us to guide you through every step of your refinance, making sure you understand the process and feel confident in your decision.

Ready to start building wealth through your home? Then we’re ready to help!